The Internal Revenue Service (IRS) recognizes this setup, making LLCs the choice for 35% of U.S. businesses, a balance of simplicity and security.

The first LLC statute in the United States was enacted in Wyoming in 1977, primarily to facilitate oil and gas ventures. However, it wasn’t until the IRS clarified the tax treatment of LLCs in the late 1980s and early 1990s that their popularity surged nationwide. The structure was designed to offer the liability protection of a corporation without the associated tax complexities for smaller businesses.

A study from Harvard Business Review confirms that LLCs shield assets better than sole proprietorships. Tax treatment depends on structure, single-member LLC for solo owners, and multi-member LLC for partnerships. LLC State Guides outline local compliance rules, while a registered agent ensures proper legal filings.

A solid LLC operating agreement keeps ownership and responsibilities clear. Filing a yearly report maintains compliance. Some LLCs prefer C Corporation taxation for lower rates. With the right setup, an LLC provides flexibility, protection, and long-term growth. This guide covers everything you need to know to form an LLC, from legal requirements to tax benefits – 2025 Guide.

Understanding This Hybrid Business Structure (LLC)

A Limited Liability Company (LLC) mixes elements of a corporation, sole proprietorship, and partnership. It shields owners from personal liability while keeping things simple. Over 35% of small businesses in the U.S. now operate as LLCs.

While the term “LLC” is primarily used in the United States, many countries have similar business structures offering comparable benefits.

Examples include the Gesellschaft mit beschränkter Haftung (GmbH) in Germany, the Société à responsabilité limitée (SARL) in France and many other European countries, and similar forms exist in various legal systems worldwide, often with slight variations in regulations and requirements. Understanding these equivalents can be crucial for businesses operating internationally.

A study from the U.S. Chamber of Commerce highlights how an LLC must file Articles of Organization to gain legal recognition. Unlike a limited partnership, it offers more freedom in taxes and management.

For startup businesses, an LLC streamlines tax returns and protects assets. It’s a flexible way to form your business with fewer legal barriers. Below is a detailed comparison to help you decide.

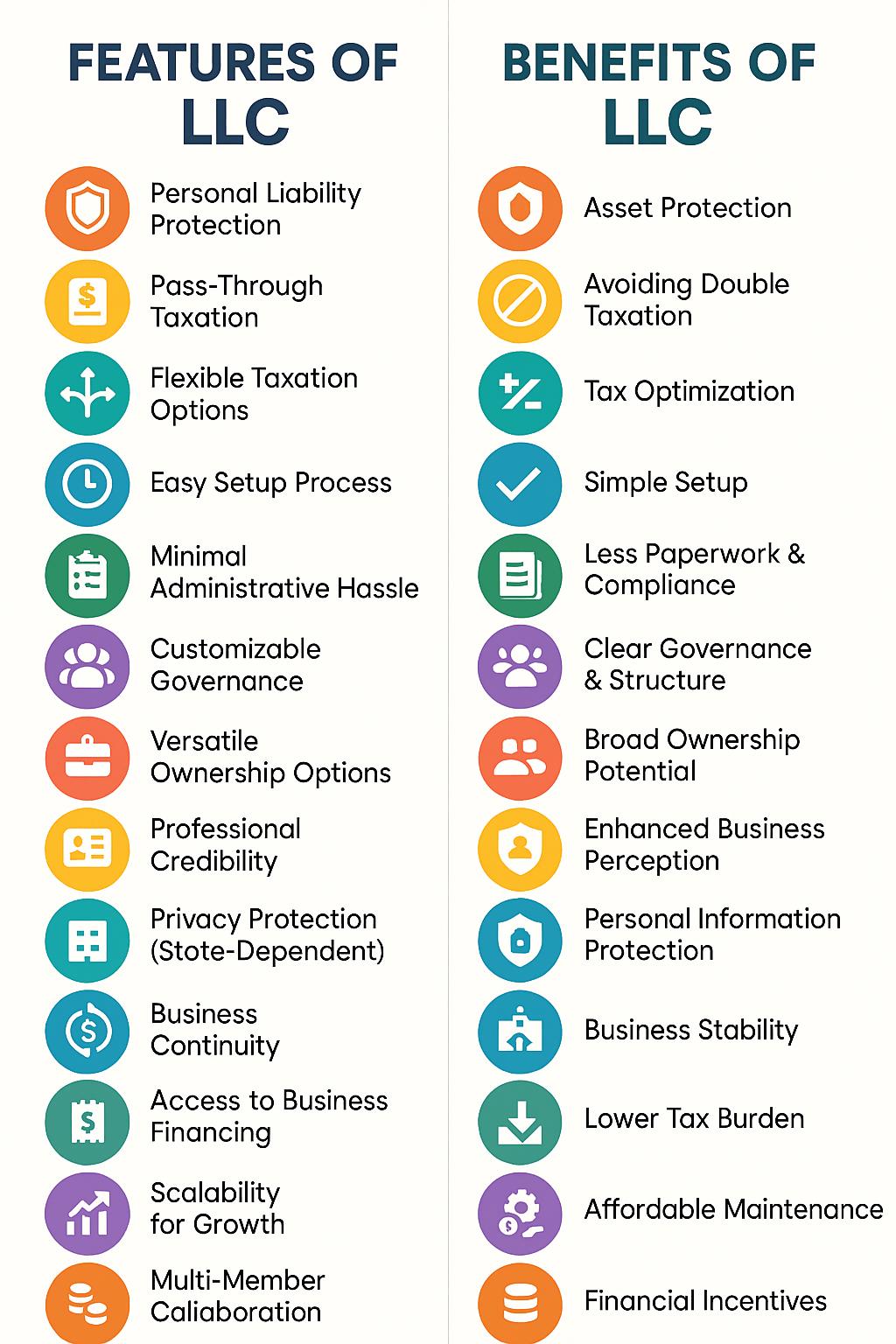

LLC Features and Benefits

Many people are familiar with the idea of forming an LLC (Limited Liability Company), but few truly understand the specific features it offers, and even fewer realize the important benefits that come with each feature.

| LLC Feature | What It Means | Direct Benefit |

|---|---|---|

| Liability Protection | Personal assets are separate | Your home & savings stay safe |

| Pass-Through Taxation | Income taxed once | Lower overall taxes |

| Flexible Tax Options | Choose S-Corp or C-Corp | Tax savings as income grows |

| Easy Setup | Online state filing | Faster business launch |

| Minimal Paperwork | Fewer reports | Less stress & admin work |

| Operating Agreement | Custom rules | Fewer disputes |

In this guide, I’ve listed not only the main features of an LLC but also explained the direct benefits associated with each one. This way, you’ll have a clear picture of how an LLC can protect, grow, and strengthen your business.

Now that you have seen a quick overview of the key features and benefits of an LLC, I will explain each one in detail. This way, you will fully understand how every feature works and how it can directly benefit you and your business.

Complete Benefits and Features – Explained in Detail

Starting a business is a big adventure, and an LLC makes the ride smoother, safer, and full of possibilities. It’s like having a smart co-pilot who protects your personal life, keeps your taxes manageable, and opens up endless growth options.

Here’s why an LLC can be a game-changer for entrepreneurs like you, with real-world perks that’ll help you thrive.

1. Feature: Personal Liability Protection

An LLC draws a clean line between your personal and business finances. If your business is in debt or sued, your personal assets, like your home, savings, and car, stay protected.

You don’t have to worry about losing everything you’ve built personally because of a business bump. That peace of mind alone makes the LLC worth it.

Benefit: Asset Protection

-

Keep creditors away from your personal property.

-

Let’s breathe easy, knowing tough business times won’t hit your personal life.

Example: If your business gets sued for a customer complaint, only the company’s assets are on the line, not your family’s house or your personal bank account.

2. Feature: Pass-Through Taxation

With an LLC, your business’s profits “pass through” straight to your personal tax return. No corporate tax bill standing in the middle. This means you’re only taxed once, as an individual, instead of getting double-taxed like big corporations do. More money stays in your pocket where it belongs.

Benefit: Avoiding Double Taxation

-

Avoids double taxation, so you keep more of your earnings.

-

Simplifies tax season with straightforward filings.

-

Boosts your profits by dodging extra tax layers.

3. Feature: Flexible Taxation Options

One of the coolest things about an LLC is its tax flexibility. You can choose to be taxed as a sole proprietor, a partnership, an S-Corp, or even a C-Corp if it suits you better. This lets you fine-tune your tax situation as your business grows, changes, and earns more.

Benefit: Tax Optimization

-

Customize your tax plan to maximize savings.

-

Reduces self-employment taxes for high earners with smart elections.

-

Adapts your tax strategy as your business evolves.

Example: If you’re pulling in strong profits, switching to S-corp status might save you thousands by reducing self-employment taxes, while still paying yourself a nice salary.

4. Feature: Easy Setup Process

Getting your LLC started is faster and easier than you might think. Most states let you file online, skip the heavy paperwork, and be official in just a few days. Compared to forming a corporation, starting an LLC feels refreshingly simple and less expensive.

Benefit: Simple Setup

-

Cuts startup legal costs compared to corporations.

-

Lets you launch your dream business without delay.

Example: In many states, you can complete your LLC registration in under an hour online and get approval within a few business days.

5. Feature: Minimal Administrative Hassle

Once your LLC is up and running, keeping it compliant is pretty easy. You don’t need to hold formal board meetings or file complicated reports every month.

Usually, you just pay a small annual fee and file a basic renewal form, and that’s it.

Benefit: Less Paperwork & Compliance

-

Frees up time to focus on growing your business.

-

Keeps compliance costs low, often just a small annual fee.

-

Streamlines operations, so you’re not buried in paperwork.

6. Feature: Customizable Governance

Running your LLC is customizable from the start. You get to set the rules with an operating agreement: who’s in charge, how decisions are made, and how the daily operations roll.

You can manage it yourself or bring in managers, whatever fits your business style and goals.

Benefit: Clear Governance & Structure

-

Clarifies roles to avoid confusion or conflicts.

-

Adapt leadership as your business grows or goals shift.

-

Keeps everyone aligned, like a playbook for success.

Example: Maybe you want to manage everything solo today, but next year, you hire a manager to help. Your operating agreement makes that transition seamless.

7. Feature: Versatile Ownership Options

LLCs are super flexible with who can own them. Individuals, corporations, and even foreign investors can be owners. You can also decide exactly how ownership changes happen, like who’s allowed to buy in or take over. That control gives you a powerful way to grow while protecting your vision.

Benefit: Broad Ownership Potential

-

Simplifies transitions, like passing the business to family or selling your share.

-

Keeps control over who joins your company.

8. Feature: Professional Credibility

Adding “LLC” to your business name instantly upgrades your image. Customers, suppliers, and investors see you as legit, serious, and trustworthy. In a world full of side hustles and pop-up businesses, looking official can make a massive difference.

Benefit: Enhanced Business Perception

-

Builds trust, making customers more likely to choose you.

-

Helps land bigger contracts or partnerships with major companies.

-

Lets you apart from less formal sole proprietors.

9. Feature: Privacy Protection (State-Dependent)

Depending on where you form your LLC, you might be able to keep your name and address off public records. States like Delaware and Wyoming offer this kind of privacy protection.

Benefit: Personal Information Protection

-

Shield your identity from public view.

-

Reduces risks like harassment or identity theft.

-

Keep your personal life low-profile for added security.

Example: In Wyoming, you can set up your LLC through a registered agent, meaning your personal name never appears in public documents.

10. Feature: Business Continuity

With the right setup, your LLC keeps going even if an owner leaves, sells their share, or passes away. Your business doesn’t have to shut down just because something changes. That stability is good for your employees, your customers, and your long-term plans.

Benefit: Business Stability

-

Ensures your business stays steady through unexpected changes.

-

Minimizes disruptions for employees and customers.

-

Build a lasting legacy you can be proud of.

11. Feature: Access to Business Financing

Banks and investors love the stability an LLC signals. You’ll find it much easier to qualify for loans, lines of credit, or outside funding compared to running as a sole proprietorship. Having an LLC can open doors you might not even realize exist yet.

Benefit: Access to Capital

-

Unlocks loans to open a new location or buy equipment.

-

Attracts investors, like angel funders for your next big product.

-

Fuels growth without leaning on your personal credit.

12. Feature: Deductible Business Expenses

Running your business comes with costs, and as an LLC, you get to write those off. Office rent, marketing campaigns, travel expenses — all potentially deductible. This lowers your taxable income and leaves you with more money to reinvest in your growth.

Benefit: Lower Tax Burden

-

Cuts your tax bill, leaving more for reinvestment.

-

Turns everyday expenses into tax savings.

-

Make every dollar spent work harder.

13. Feature: Scalability for Growth

As your dreams get bigger, your LLC can grow right alongside you. And if you ever need to raise big capital or go public, you can convert to a corporation without starting over from scratch. You’re building on a foundation that’s flexible enough to handle big leaps.

Benefit: Growth Flexibility

-

Support your business as it scales, no overhaul needed.

-

Keep your foundation strong while you chase bigger goals.

-

Saves time and costs compared to starting fresh.

14. Feature: Multi-Member Collaboration

LLCs make partnerships and collaborations super easy. You can team up with other owners, combining skills, resources, and capital. This not only spreads the risk but also sparks new ideas and innovation that solo founders might miss.

Benefit: Affordable Maintenance

-

Sparks innovation through shared expertise.

-

Splits the workload and financial risk among partners.

-

Attracts talented co-owners to drive growth.

15. Feature: State-Specific Incentives (Where Available)

Depending on your state, there could be extra perks waiting for you. Some states offer tax breaks, grants, or even mentorship programs just for small LLCs. It’s worth checking local programs to see if you can score some serious startup advantages.

Benefit: Financial Incentives

-

Slashes startup costs with local tax perks.

-

Provides access to grants or mentorship programs.

-

Gives your business a head start, depending on your state.

An LLC is like a Swiss Army knife for entrepreneurs, protective, flexible, and ready for anything. It keeps your personal life safe, your taxes manageable, and your growth potential sky-high. Whether you’re just starting or scaling up, an LLC gives you the tools to build something lasting.

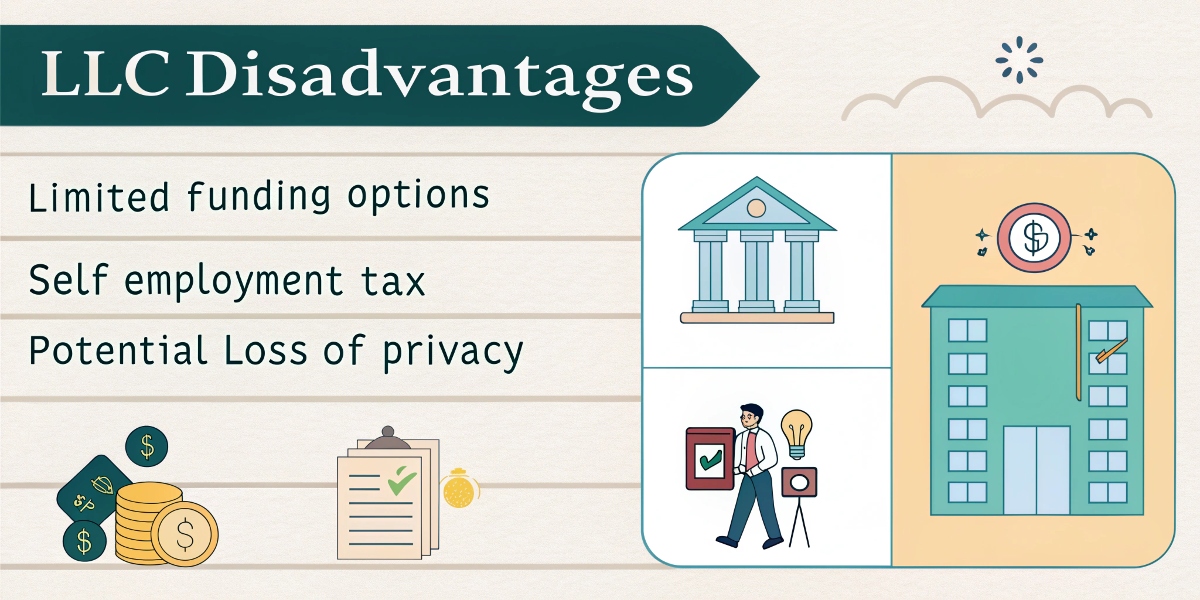

LLC Disadvantages:

While LLCs offer numerous advantages, they also come with some challenges to consider before making a decision.

Self-Employment Taxes

LLC members must pay the full Social Security and Medicare taxes on their income, unlike corporate employees, whose employers cover half of these contributions.

Formation & Ongoing Costs

Registering an LLC typically involves higher fees than sole proprietorships, with some states requiring annual renewal fees and franchise taxes.

While these challenges exist, they are manageable with the right business strategy. If flexibility and liability protection outweigh the drawbacks, forming an LLC remains a powerful choice for entrepreneurs looking to establish a strong foundation for growth.

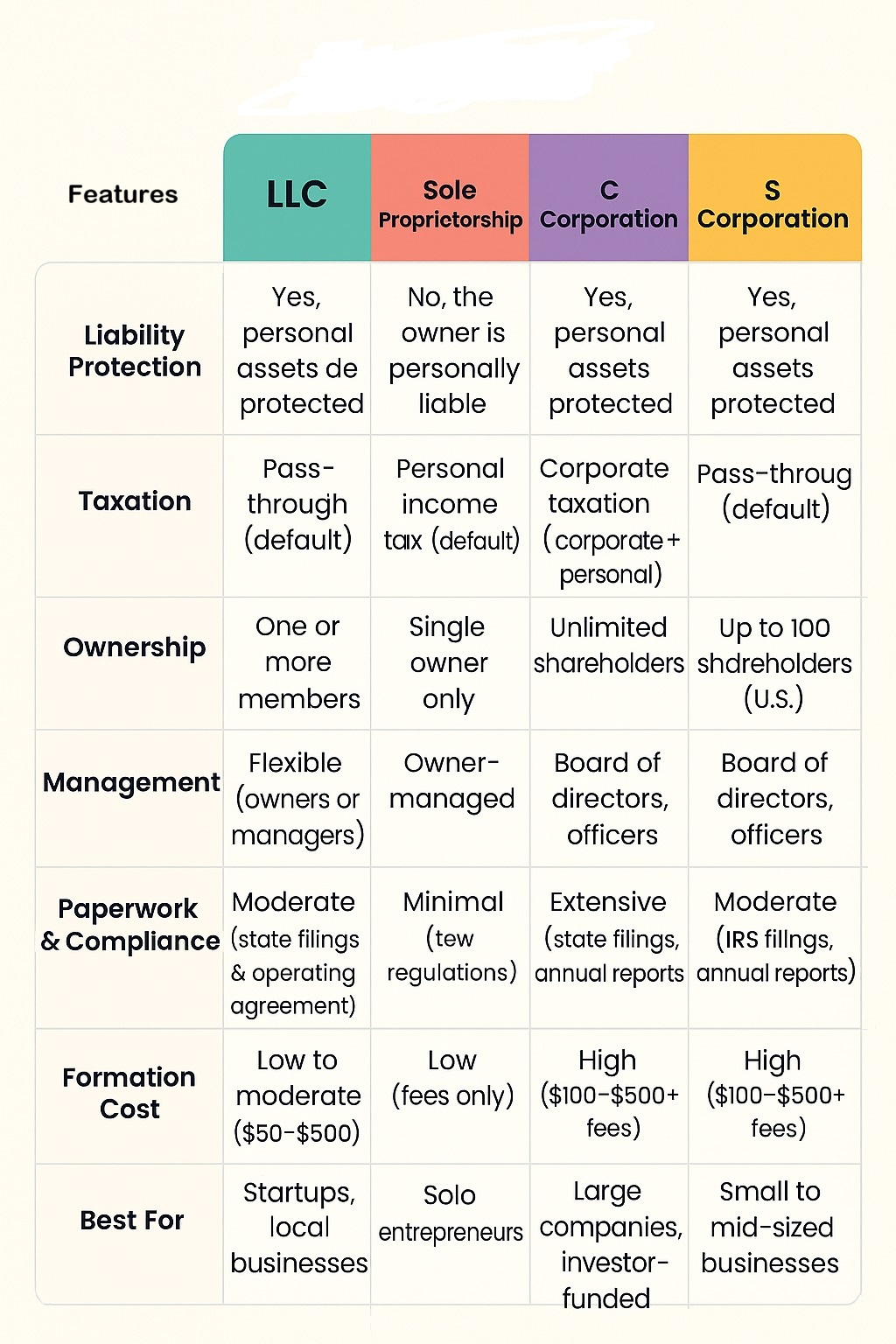

LLC vs. Sole Proprietorship vs. Corporation

Choosing the right business structure is a major decision for any entrepreneur. LLCs, sole proprietorships, and corporations each offer different levels of protection, taxation, and flexibility.

| Feature | LLC | Sole Proprietorship | Corporation |

|---|---|---|---|

| Personal Asset Protection | ✅ Yes | ❌ No | ✅ Yes |

| Pass-Through Taxation | ✅ Yes (default) | ✅ Yes | ❌ No |

| Double Taxation | ❌ No | ❌ No | ✅ Yes |

| Ease of Setup | Easy | Very Easy | Complex |

| Ongoing Compliance | Low | Very Low | High |

| Best For | Small businesses, startups | Solo freelancers | Large companies |

While sole proprietorships are simple and easy to set up, they offer no personal liability protection.

Corporations provide strong protection but come with more regulations and double taxation. An LLC strikes a balance, giving you personal asset protection with flexible management and simpler taxes.

This breakdown makes it easy to see why LLCs are a popular choice, offering protection like a corporation but flexibility like a sole proprietorship.

LLC vs. Trademark: Key Differences

LLC vs. Trademark: Key Differences

Tax Benefits of an LLC: Save Smarter, Grow Faster

An LLC isn’t just a business structure it’s a tax-saving powerhouse for small business owners. Millions of entrepreneurs now choose LLCs for their flexibility and tax perks, according to IRS data (2023). You dodge corporate taxes, claim bigger deductions, and tailor your tax strategy to fit your goals. Here’s how an LLC puts more money back in your pocket.

Pass-Through Taxation

Your LLC’s profits skip corporate taxes and land straight on your personal return. In no-income-tax states like Texas or Florida, you save even more.

Why It’s Great:

-

Avoids double taxation and boosts take-home profits.

-

Simplifies filings with just a personal tax return (Schedule C for single-member LLCs).

-

Maximizes savings, especially in low-tax states.

Flexible Tax Options

Choose how your LLC is taxed as a sole proprietor, partnership, S corporation, or C corporation. Electing S-Corp status, for example, lets you pay yourself a salary and take distributions to cut self-employment taxes.

Why It’s Great:

-

Customize your tax plan to minimize what you owe.

-

Saves big on self-employment taxes (15.3% on net earnings) if you’re a high earner.

-

Adapts as your business grows.

Startup and Organizational Cost Deductions

Deduct up to $5,000 in startup costs and $5,000 in organizational costs right away if total expenses stay under $50,000 (IRS, 2024).

Why It’s Great:

-

Lowers your taxes right from day one.

-

Offsets the cost of launching your business.

-

Frees up cash to scale faster.

Home Office Deductions

Work from home? You can deduct office costs using the simple method ($5 per square foot, up to $1,500) or actual expenses like rent and utilities.

Why It’s Great:

-

Turn your home into a tax-saving zone.

-

Makes filing easy with the $1,500 standard deduction.

-

Cuts taxable income to keep profits higher.

Business Expense Deductions

Write off everyday business costs marketing, travel, equipment, utilities to lower your taxable income.

Why It’s Great:

-

Slashes your tax bill with routine expenses.

-

Let’s reinvest savings back into your business.

-

Make every dollar spent work harder.

Qualified Business Income (QBI) Deduction

Deduct up to 20% of business income under Section 199A. For 2025, the phase-out starts around $191,950 (single) or $383,900 (married filing jointly).

Why It’s Great:

-

Cuts your taxable income by up to 20%.

-

Rewards you just for owning a business.

-

Boosts profits for future growth.

Self-Employment Tax Savings

By default, you pay 15.3% in self-employment taxes. Electing S-corp status lets you balance salary (taxed) and distributions (not taxed for self-employment).

Why It’s Great:

-

Saves thousands on Medicare and Social Security taxes.

-

Balances compliance with savings.

-

Put real cash back in your pocket.

Retirement Plan Contributions

Open a SEP-IRA or solo 401(k) and deduct up to $69,000 in 2025 (IRS limits) to save on taxes while building retirement wealth.

Why It’s Great:

-

Lowers taxes while growing your uture nest egg.

-

Rewards smart, long-term financial planning.

-

Let you invest pre-tax dollars for maximum impact.

Health Insurance Deductions

Deduct health insurance premiums for yourself, your spouse, and dependents (IRS Publication 535).

Why It’s Great:

-

Offsets healthcare costs with real savings.

-

Makes staying insured more affordable.

-

Protect your health and your wallet.

State-Specific Tax Incentives

Many states offer LLCs tax credits or exemptions, especially for job creation or operating in opportunity zones. No-income-tax states like Nevada or Wyoming boost savings even further.

Why It’s Great:

-

Cuts taxes with local incentives.

-

Maximizes profits in business-friendly states.

-

Unlocks new credits to fund growth.

An LLC acts like your financial sidekick, helping you dodge corporate taxes, rack up deductions, and hold onto more profits. From startup deductions to retirement planning, it’s built to make your business journey smarter and stronger.

Why Choose an LLC Over Other Business Structures?

An LLC provides tax flexibility and liability protection is essential for a single member LLC being incorporated, making them ideal for startup businesses. Unlike a C Corporation, it avoids double taxation and keeps ownership simple.

A report from the U.S. Small Business Administration (SBA) found that an LLC usually costs under $500 to register. You can control the business without dealing with shareholders.

-

No corporate double taxation

-

Easier to register your business

-

More control over decisions

-

LLC utilizes managers for flexibility

If you’re looking to choose a business setup that protects assets and stays hassle-free, an LLC is a smart move.

Why Choose an LLC Instead of DBA?

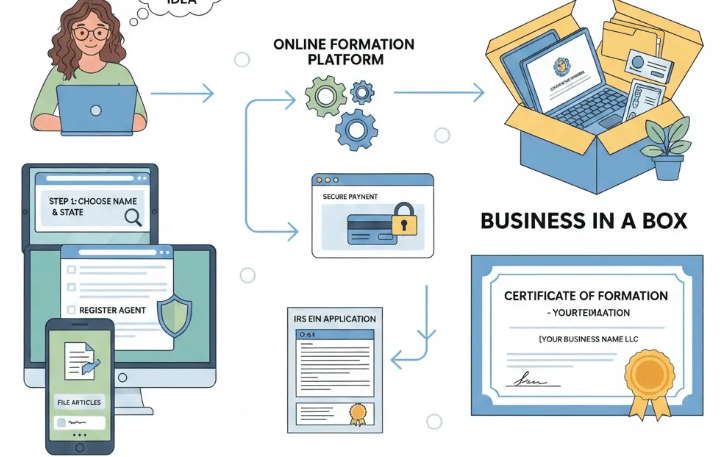

How To Start an LLC – Step-by-Step Guide

Starting a business entity like an LLC requires legal paperwork, compliance, and smart planning. Over 70% of small business owners choose an LLC for liability protection and tax benefits. Each state has unique rules, but the general steps remain the same; pick a name, file documents, and appoint a registered agent.

Creating an LLC is easier than many people think. It usually starts with choosing a unique business name and filing Articles of Organization with your state.

| Step | Action Required | Who Handles It |

|---|---|---|

| Step 1 | Choose business name | Owner |

| Step 2 | File Articles of Organization | State |

| Step 3 | Appoint Registered Agent | Owner / Service |

| Step 4 | Create Operating Agreement | Owner |

| Step 5 | Get EIN | IRS |

| Step 6 | Open Business Bank Account | Bank |

You’ll also need to appoint a registered agent and create an operating agreement to define how your LLC will run.

Once you get your approval, you can obtain an EIN and officially open for business. I’ve also written a detailed guide that walks you through every step clearly and simply.

Choose a Business Name and Verify Availability

-

Ensure the name meets state filing agencies rules.

-

Some states require a registered “doing business” name.

File Articles of Organization

-

Submit articles of organization LLC forms to the Secretay of State

-

.List the LLC members, business address, and structure

-

Pay the state’s filing fee and wait for approval.

What Mail Can I Expect After Registering a Business?

Appoint a Registered Agent

-

A registered agent receives legal documents on behalf of your LLC.

-

This can be an LLC owner, attorney, or registered agent services

-

Must have a physical address in the state where the LLC is formed.

Draft an Operating Agreement

-

Defines ownership of an LLC, decision-making, and dispute resolution.

-

Not all states require it, but it prevents conflicts among LLC and the members.

-

Helps maintain your business’s legal structure.

Obtain an EIN from the IRS

-

Apply for an Employer Identification Number (EIN) online for free.

-

Required for tax purposes, hiring employees, and opening a business account.

-

The IRS will treat an LLC based on its chosen tax classification.

Setting up an LLC ensures legal protection and credibility. According to the IRS, an LLC can choose to be taxed as a C corporation, offering unique tax advantages. Getting it right f rom the start keeps your business compliant and future-ready.

Legal and Regulatory Requirements for Operating an LLC

An LLC being incorporated comes with legal responsibilities. States require annual filings, a resident agent , and franchise tax payments where applicable. Keeping up with state rules ensures the business is operated without legal disruptions.

A study from the National Small Business Association highlights that businesses adhering to state compliance laws reduce legal risks by 40%. The registered “doing business” status legally protects owners from unexpected liabilities. Each state has unique rules, making professional guidance essential.

Key Compliance Factors:

Annual Filings and Reports

Every LLC must file an Annual Report with the state to remain active. This report updates key business details, including ownership, management, and resident agent. Some states impose penalties or automatic dissolution if filings are missed. Staying compliant avoids legal trouble and keeps the company in good standing.

Annual Reporting vs. Taxes: Key Differences for Businesses

Franchise Taxes (Where Applicable)

Several states impose fees on franchise activities designated as business licenses for operating privileges. Under California state law businesses need to pay at minimum $800 per year. Franchise taxes are imposed with different conditions based on revenue levels and structural and geographical locations. Not paying taxes can lead to both interest fees and potential forfeiture of legal protection.

Maintaining a Registered Agent

LLCs must have a registered agent to handle official state communications and legal notices. This ensures lawsuits or compliance notices are received and addressed on time. A reliable agent helps avoid missed deadlines and legal complications. Businesses can hire professional agents for added security.

Compliance with State Requirements

Each state has different rules governing LLCs. Some require publication of formation notices, while others mandate business licenses and specific permits. It’s essential to check jurisdictional rules to avoid fines or operational restrictions. Regular legal checkups help businesses stay compliant.

Beneficial Ownership Information (BOI) Report: How to Submit It

Importance of Adhering to the Operating Agreement

Operating Agreements specify rights belonging to the owners along with profit-sharing mechanics and rules for running the business. Not following the document can result in internal disagreements as well as possible legal complications. Well-drafted agreements both enable easy determination of decisions and defend members from potential financial damages.

LLCs differ from a limited liability partnership, offering flexibility and protection. Aligning with the goals of the business secures long-term success. Compliance isn’t just a rule, it’s the foundation of financial and legal security.

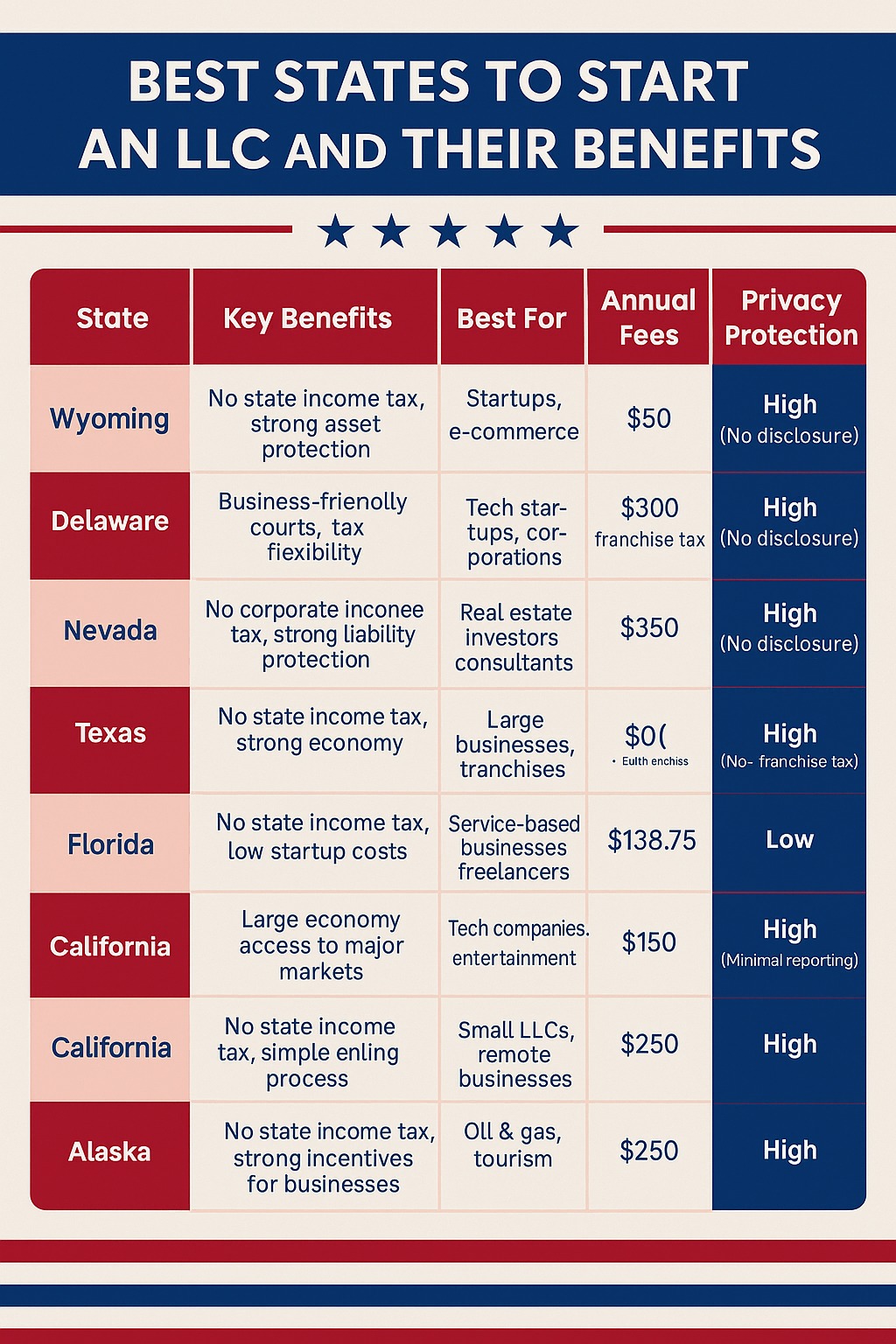

Costs of Forming an LLC

LLC costs depend on location. Some states charge higher filing fees, while others offer tax benefits. Here’s a breakdown:

According to the U.S. Small Business Administration, states like Wyoming and Delaware have lower LLC formation service provider costs. Meanwhile, California and New York have higher annual LLC maintenance costs.

| State | Filing Fee | Annual Fee |

|---|---|---|

| Wyoming | $100 | $60 |

| Delaware | $110 | $300 |

| Texas | $300 | $0 |

| Florida | $125 | $138 |

| California | $70 | $800 |

Plan for startup formation costs by comparing filing fees by state. Submitting an LLC order form early avoids penalties. Keeping up with LLC resources ensures compliance.

Common Mistakes to Avoid When Registering an LLC

| Mistake | Risk | How to Avoid |

|---|---|---|

| No Operating Agreement | Ownership disputes | Draft one early |

| Missing Annual Filings | Penalties or dissolution | Set reminders |

| Mixing Finances | Lose liability protection | Separate bank account |

| Wrong Tax Election | Higher taxes | Talk to a tax expert |

Forming an LLC is simple, but common mistakes can lead to legal or financial troubles. Avoid these pitfalls:

-

Skipping an LLC operating agreement – Leads to ownership disputes.

-

Failing to maintain compliance – Results in penalties and legal issues.

-

Mixing personal and business finances – Puts liability protection at risk.

-

Missing state business filing deadlines – Can dissolve your LLC.

-

Choosing the wrong tax classification – Affects how your LLC is taxed.

A Cornell Law School study emphasizes that strong business compliance laws protect business owners. Ensuring proper LLC financial separation keeps liabilities clear.

To stay compliant :

-

Follow the tax filing mistakes for LLCs guidelines.

-

Keep your LLC active with timely filings.

-

Understand the company’s decision-making process for smooth operations.

Taking the right steps ensures your LLC remains legally sound and financially secure.

Differences Between LLCs, Partnerships, and Corporations

Choosing the right business type matters. A Limited Liability Company (LLC) offers liability protection for business owners and tax flexibility. A corporation and a partnership differ, corporations attract investors but face double taxation, while partnerships share liability. The U.S. The Small Business Administration notes that over 35% of startups prefer LLCs.

A study from the U.S. Chamber of Commerce highlights that the formation of an LLC ensures a separate entity, protecting owners financially. Unlike a sole proprietorship, an LLC is owned by members who manage operations with fewer regulations.

For large-scale growth, a C Corporation and S Corporation work best, while general and limited partnerships (LPs) suit smaller ventures. Before transacting business, consider taxation, management, and risk.

LLC vs. Partnership: Key Differences

| Area | LLC | Partnership |

|---|---|---|

| Liability Protection | Yes | No |

| Tax Flexibility | High | Limited |

| Ownership | 1 or more | 2 or more |

| Legal Risk | Lower | Higher |

An LLC shields the owner of an LLC from business debts, while partnerships expose owners to shared liability. A single-member limited liability company has one owner, whereas partnerships require at least two. LLCs also provide LLC tax flexibility, allowing businesses to optimize their tax structure.

Key Differences:

-

Liability Protection LLC owners aren’t personally responsible for debts, but partners are.

-

Taxation Partnerships have pass-through taxation for LLCs, but LLCs can choose corporate taxation.

-

Ownership LLCs can be single or multi-member; partnerships always require multiple owners.

-

Legal Compliance: States have different rules on how an LLC will be doing business.

Case Study: A marketing agency began as a partnership before creditors attacked business assets when one partner suffered from financial troubles. The owners protected their company by converting to LLC status to obtain personal asset protection alongside tax advantages.

LLC vs. Corporation (C Corp and S Corp)

A corporation or C corporation follows a rigid structure with double taxation, while an LLC being incorporated is a misconception, LLCs register but don’t follow corporate rules. Members of the LLC manage operations more flexibly.

Key Differences:

-

Taxation: A corporation or C corporation is taxed at both corporate and personal levels, while LLCs can opt for pass-through taxation.

-

Ownership Structure Members of the LLC own and manage the business, while corporations have shareholders and boards.

-

Compliance Requirements Corporations require bylaws and formalities, while LLCs are more flexible.

-

Formation Businesses must state the LLC when registering for legal recognition.

Case Study: A software startup formed as an LLC for tax flexibility. As it grew, investors required a corporate structure, so the company elected to be treated as a corporation, unlocking venture capital funding and scaling opportunities.

How Many Shares Should My Corporation Have?

LLC State Guides: What You Need to Know

Choosing the right LLC state impacts taxes, privacy, and compliance. The states of Wyoming and Delaware, along with Nevada, provide business-conducive laws coupled with reduced filing expenses and stronger protection of LLC profits.

Your new LLC may also need to comply with business entity-level rules, ensuring smooth operations. If your LLC is represented in multiple states, you may need to register as a foreign LLC for legal compliance.

Benefits of forming an LLC in California

In-State vs. Delaware: Where Should You Establish Your LLC?

State-Specific Filing Requirements

Each state sets different LLC formation costs and compliance regulations. Before forming a business, check:

-

Annual report fees: Some states require yearly filings.

-

Tax treatment: A disregarded entity or single-owner llc may qualify for different taxation.

-

Licensing requirements: Some businesses need extra permits.

A domestic LLC with at least two members may have different tax obligations than an LLC with only one member. Understanding how the state handles business filings is crucial for compliance.

How to Register as a Foreign LLC

If your LLC is often doing business across states, registration is required. Steps include:

-

Appointing a registered agent in the new state.

-

Filing a Certificate of Authority to legally operate.

-

Paying additional state filing fees for compliance.

Some states require an LLC to be “incorporated” elsewhere to register as a foreign LLC. Whether your business is a separate business or a professional limited liability company, staying compliant ensures smooth operations.

LLC Resources – Where to Find Help and Support

Accurate information is crucial when forming an LLC. The IRS, state business portals, and Secretary of State offices provide up-to-date details on registration and compliance. Using these official sources ensures you follow state-specific rules without errors.

-

IRS website: EIN applications and tax classification guidelines.

-

State portals: Direct access to formation documents.

-

Secretary of State offices: Business name availability checks.

A U.S. Small Business Administration study confirms that proper state filings reduce registration mistakes. The IRS website also provides tax structure guidance, ensuring compliance. Bookmark these sites and use live chat options many states offer to streamline the process.

BusinessRocket is an online LLC formation company that provides full support, handles all legal work, and forms your LLC for you.

Who Should Choose an LLC

| Business Type | Is LLC a Good Fit? |

|---|---|

| Freelancers | ✅ Yes |

| Startups | ✅ Yes |

| Real Estate Investors | ✅ Yes |

| Large Public Companies | ❌ No |

| Short-Term Projects | ⚠️ Maybe |

LLC for Real Estate: Why an LLC is the Best Bet for Real Estate

Company Registration in USA for Non-Residents: Complete Guide

FAQ’S

What does an LLC actually do?

Think of an LLC as a legal wall between you and your business. It keeps your personal stuff like your house, car, and savings—safe from business debts or lawsuits. If the business hits a snag, your personal assets usually stay protected.

What is the general purpose of an LLC?

An LLC is all about giving small business owners a safety net. It protects your personal finances from business risks while keeping things simple and flexible to run.

What is the biggest benefit of an LLC?

The star of the show is personal liability protection. If your business gets sued or can’t pay its debts, you’re not personally on the hook. Your personal bank account stays out of the mess.

Is LLC good or bad?

For most small businesses, an LLC is a solid choice. It gives you strong legal protection without the headaches of running a full-blown corporation. It’s like a sweet spot for simplicity and security.

How does an LLC make you money?

An LLC isn’t a cash machine, it’s just the legal setup for your business. You make money by selling products or services, just as any business. The LLC just gives you a formal structure under which to work.

How do I pay myself from my LLC?

If you’re a single-member LLC, it’s super cool. You take an owner’s draw—just move money from your business account to your personal one. Just make sure the business has enough cash to cover its bills!

Why should I choose an LLC instead of a sole proprietorship or corporation?

An LLC beats a sole proprietorship because it protects your personal assets if things go wrong. Compared to a corporation, it’s way easier to manage no endless paperwork or formal board meetings. It’s a great middle ground.

Does an LLC protect my personal assets?

Yes, it does, as long as you play it smart. Keep your business and personal finances separate (no buying personal stuff with the business card!) and avoid personally guaranteeing business debts. Do that, and your personal stuff should stay safe.

How is an LLC taxed?

By default, an LLC is a pass-through, so your business profits go straight to your personal tax return. You can also opt to be taxed like an S corp or C corp if that works better for your situation. A tax pro can help you decide.

How much does it cost to start and maintain an LLC?

It varies by state, but starting an LLC usually costs $50–$500. Then there are annual fees or reports, typically $50–$300. Check your state’s rules since some are pricier than others.

What are the steps to form an LLC?

Here are 4 steps:

-

Choose a unique business name and make sure it’s available.

-

File Articles of Organization with your state.

-

Grab an EIN (like a business Social Security number) from the IRS.

-

Write up an operating agreement to lay out how your LLC will run. And you’re off to the races!

Do I need a registered agent for my LLC?

Yup, every LLC needs one. A registered agent handles legal documents for your business. It can be you, a buddy, or a professional service just make sure they’re reliable.

Can a single person own an LLC?

Absolutely! Single-member LLCs are super common and totally legal in every state. Perfect for solo entrepreneurs.

What are the disadvantages of an LLC?

It’s not perfect. Some states charge steep annual fees, and you might deal with self-employment taxes unless you switch up your tax status. A quick chat with an accountant can help you navigate this.

In which state should I form my LLC?

Your home state is usually the best. Forming an LLC in another state (like Delaware or Wyoming) might sound tempting, but it can mean extra costs and paperwork unless your business is actually operating there.

Minnesota Secretary of State | Business Entity Search July 7, 2026 - Home » What is Limited Liability Company (LLC) – How it Works 2026 GuideMinnesota Business Entity Search in 2026 Minnesota business entity search tool is free, instant, and official. Run a state of Minnesota business entity search before you start a new business, verify a partner, or claim a name. Fastest National Processing Times! REGISTER …

Minnesota Secretary of State | Business Entity Search July 7, 2026 - Home » What is Limited Liability Company (LLC) – How it Works 2026 GuideMinnesota Business Entity Search in 2026 Minnesota business entity search tool is free, instant, and official. Run a state of Minnesota business entity search before you start a new business, verify a partner, or claim a name. Fastest National Processing Times! REGISTER …Minnesota Secretary of State | Business Entity Search Read More »

Business Entity Search – Missouri Secretary of State June 25, 2026 - Home » What is Limited Liability Company (LLC) – How it Works 2026 GuideMissouri Business Entity Search in 2026 – SOS Find and verify Missouri businesses using the Secretary of State’s official search tool. Look up LLCs, corporations, partnerships, and sole proprietorships in 2022. Trustpilot Fastest National Processing Times! REGISTER AN LLC The Missouri …

Business Entity Search – Missouri Secretary of State June 25, 2026 - Home » What is Limited Liability Company (LLC) – How it Works 2026 GuideMissouri Business Entity Search in 2026 – SOS Find and verify Missouri businesses using the Secretary of State’s official search tool. Look up LLCs, corporations, partnerships, and sole proprietorships in 2022. Trustpilot Fastest National Processing Times! REGISTER AN LLC The Missouri …Business Entity Search – Missouri Secretary of State Read More »

Virginia Business Search in 2026 – Check Name Availability June 11, 2026 - Home » What is Limited Liability Company (LLC) – How it Works 2026 GuideVirginia Business Entity Search in 2026 – SCC The Virginia State Corporations Commission (SCC) offers an online search tool to find Virginia’s registered businesses. Users can search by business name using standard or advanced filters. Trustpilot Fastest National Processing Times! REGISTER AN …

Virginia Business Search in 2026 – Check Name Availability June 11, 2026 - Home » What is Limited Liability Company (LLC) – How it Works 2026 GuideVirginia Business Entity Search in 2026 – SCC The Virginia State Corporations Commission (SCC) offers an online search tool to find Virginia’s registered businesses. Users can search by business name using standard or advanced filters. Trustpilot Fastest National Processing Times! REGISTER AN …Virginia Business Search in 2026 – Check Name Availability Read More »